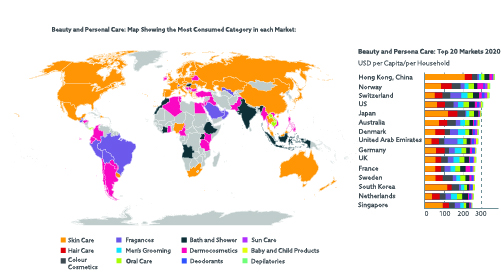

Market overview

In recent years there has been a significant increase in the development of the ‘ingestible beauty’ trend, however, a more common and ‘consumer friendly’ term has taken precedence. ‘Beauty-from-within' speaks to the modern consumer and has grown in popularity. Clinical research has shown that beauty is not skin deep, it is an integrated approach including both skincare and a healthy diet. The surge of consumers focusing on self-care amid the pandemic has only accelerated the emergence of wellness as a holistic trend extending to traditional beauty areas such as skincare. Including clinically-proven botanical ingredients and using the highest standard of practice (ICH-GCP) will significantly increase the success of a product, which will be further addressed in the latter of this article. Furthermore, like many other categories, the pandemic has accelerated the beauty industry’s shift to e-commerce as brick-and-mortar locations have had to close. In the US, personal care and beauty online sales totaled an astonishing $62.6B last year, up from $53.1B in 2019, per CB Insights.

Market growth & the future of Skin

The global beauty & personal care industry was worth a staggering USD 487.4 billion in 2020, of this the skincare industry was worth USD 139.6 billion. Skin care’s 2021 growth is predicted to outpace all other categories, driven by Asia-Pacific, in particular. The post covid-19 era will result in a direction of sustainability focused and digitally savvy brands, as well as those that offer affordable, clinically validated and wellness orientated solutions. While projections for growth vary, most agree it will continue to advance at a 5%-to-7% compound-annual-growth-rate to reach or exceed $800 billion by 2025.

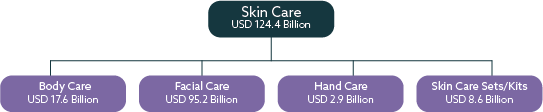

Skin Care Industry, at a glance

Wellness Vs Symptomatic health claims

A report from Lumina Intelligence identified two segments of consumers depending on the application reason: wellness versus symptomatic. For example, in Eczema, the leading sub-area is psoriasis with 2,000 average monthly searches. At the keyword level of this sub-group, searches for the term “best probiotic brand for psoriasis” have shrunk by nearly 80% in the last 24 months. However, “best probiotics strain for psoriasis” is growing exponentially (1,300%). Is this a shift in the way consumers are seeking out recommendations? And does this open a gap for suppliers to influence the end user with content on their strains? In Acne, “hormonal” and “fungal” acne appear in high-growth niche quadrant. Despite Acne as a whole group having low growth in comparison to others, there are still high-growth opportunities worth exploring. These “cause” searches are not necessarily people taking probiotics to alleviate acne, but it tells us that these symptom consumers are wary of the impact of any dietary changes. Therefore, they might need more convincing probiotic efficacy – no matter what they are taking them for. The report from Lumina also highlighted those cosmetic products with probiotics saw the largest growth in consumer interest of 113% in the 1st half of 2020. Consumer online engagement with probiotic cosmetics grows 8 times faster in % terms than that with probiotics supplements in NA and 2.5 times faster in APAC.

Clinical Research Trends

To fully understand the cosmetic market of products whose claims have been scientifically validated, the Atlantia team looked at Clinicaltrials.gov and downloaded all trials under the keyword “cosmetics” on the 26/08/2021. Just trials carried out with cosmetic products, dietary supplements, probiotics, and combinational products were included (n=89). Clinical trials tackling the skin with biological, medical devices, drugs and chirurgical interventions were excluded. The variables used to segment the data were study type (interventional/observational), condition researched and product type of the intervention if any (dietary supplement, cosmetic product, combinational product). By study type, 78.65% of studies carried an intervention while 21.35% were merely observational. Interestingly, there was a considerable variation on average sample sizes on intervention studies (89 participants) versus observational studies (2607 participants). This makes sense as there are different formulas of sample size calculation for different types of variables measured in distinct study designs, namely descriptive, epidemiological, comparative, and interventional research studies.1 (Kumar 2020) By condition researched, many diverse conditions were recurrent as study endpoints.

Straight from our experts: Where do you see the future of skin research?

“There has been a shift away from negative ‘anti-ageing’ claims in the Skin care industry and the focus is now on achieving healthy skin and ‘well ageing’ which is a more holistic approach to skin care. I believe that the future of skin research will be focused towards skin health and will delve further into the gut-skin-brain connection. Customised skincare is also a huge trend, and I will be interested to see more research studies exploring how we can look at our genetic pre-disposition and utilise this knowledge to take a pro-active approach in targeting individual skin health and ageing concerns.”